SR&ED In Federal Budgets (Summary)

Part 5: New Government, New Innovation Agenda (2016-present)

Background

After a dramatic federal election, the Liberal party won a surprise majority, taking 184 of the 338 seats in parliament with representatives in every province and roughly 40% of the popular vote. With the new leadership came a clear attempt to “take the reigns” in regards to innovation.

2016 Federal Budget

Liberal Majority under Prime Minister Justin Trudeau

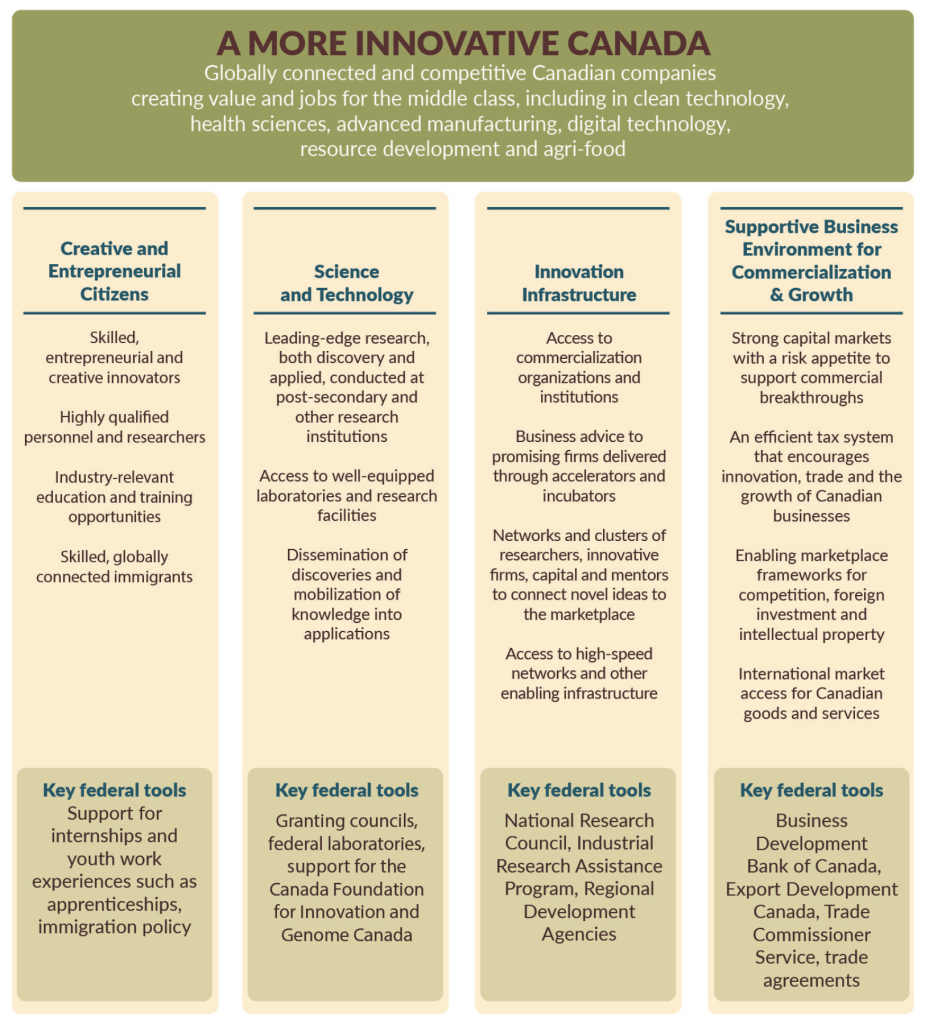

Innovation Funding in the Budget: An Overview

In his budget speech, Finance Minister Bill Morneau stated that support for innovative sectors would help to “ensure Canada is at the forefront of technological advancement in the 21st century.”27 Budget 2016 promises to make this goal a reality by offering support for innovative research and post-secondary institutions, expanding access to business development services, creating so-called “innovation hubs”, and encouraging commercialization in innovative sectors.

A More Innovative Canada” from federal budget 2016 28

Highlight’s from the budget’s innovation funding initiatives include:

- $2 billion over three years for targeted, short-term infrastructure projects under the Post-Secondary Institutions Strategic Investment Fund, to be used for “enhancing and modernizing research and commercialization facilities on Canadian campuses, as well as industry-relevant training facilities at college and polytechnic institutions, and projects that reduce greenhouse gas emissions”;

- $95 million per year in new annual funding for “discovery research”, including $30 million for the Natural Sciences and Engineering Research Council (NSERC);

- $41.5 million to support the “rehabilitation and modernization of select Agriculture and Agri-Food Canada and Canadian Food Inspection Agency research stations and laboratories” in select provinces;

- Up to $800 million to support creation of innovation networks and clusters; and

- An additional $50 million in 2016-17 to increase services offered by the National Research Council’s Industrial Research Assistance Program (IRAP)29

However, you may notice that these “highlights” do not include any mention of the Scientific Research and Experimental Development (SR&ED) program. Why is this?

A Surprising – and Significant – Change in 2019

A significant announcement has been made in relation to SR&ED: repealing the use of taxable income as a factor in determining a CCPC’s annual expenditure limit for the purpose of the enhanced SR&ED tax credit. As a result, small CCPCs with taxable capital of up to $10 million will benefit from unreduced access to the enhanced refundable SR&ED credit regardless of their taxable income.

Scientific Research and Experimental Development Program

Under the Scientific Research and Experimental Development (SR&ED) tax incentive program, qualifying expenditures are fully deductible in the year they are incurred. In addition, these expenditures are eligible for an investment tax credit. The rate and level of refundability of the credit vary depending on the characteristics of the firm, including its legal status and its size 43.

- For all corporations other than Canadian-controlled private corporations (CCPCs) and for unincorporated businesses, a 15-per-cent non-refundable tax credit is available on all qualifying SR&ED expenditures.

- For CCPCs, a fully refundable enhanced tax credit at a rate of 35 per cent is available on up to $3 million of qualifying SR&ED expenditures annually. This expenditure limit for a taxation year is gradually phased out based on two factors, which apply on the basis of an associated group.

- The expenditure limit is reduced where taxable income for the previous taxation year is between $500,000 and $800,000.

- The expenditure limit is also reduced where taxable capital employed in Canada for the previous taxation year is between $10 million and $50 million.

- Qualifying expenditures in excess of a CCPC’s expenditure limit are eligible for the 15-per-cent tax credit. Unused SR&ED credits earned at this rate may be partially refundable depending on the CCPC’s taxable income and taxable capital.

Table 5 presents the amount of SR&ED credits on $3 million of SR&ED expenditures at specific levels of taxable capital and taxable income under the current rules. In particular, it illustrates how these credits can be affected by a relatively small change in the amount of taxable income for firms within the phase-out range.

For example, a CCPC that spends $3 million on qualifying SR&ED expenditures in a taxation year, and that has $500,000 of taxable income and $10 million of taxable capital in the previous taxation year, is eligible for the 35-per-cent refundable SR&ED credit on all of its expenditures, resulting in a fully refundable credit of $1.05 million. If the corporation’s taxable income for the previous taxation year were $600,000 instead, the total SR&ED tax credits earned would have been $850,000 (of which $700,000 would have been refundable). For this CCPC, a $100,000 increase in taxable income would have resulted in a $200,000 reduction in SR&ED tax credits.

Budget 2019 proposes to repeal the use of taxable income as a factor in determining a CCPC’s annual expenditure limit for the purpose of the enhanced SR&ED tax credit. As a result, small CCPCs with taxable capital of up to $10 million will benefit from unreduced access to the enhanced refundable SR&ED credit regardless of their taxable income. As a CCPC’s taxable capital begins to exceed $10 million, this access will gradually be reduced as shown in the highlighted column in Table 5.

This change will provide a more predictable phase-out of the enhanced SR&ED credit rate, which will more effectively support growing small and medium-sized firms as they scale up.

This measure will apply to taxation years that end on or after Budget Day 44.

This change comes as a surprise – in the last decade, the changes have focused on reducing the amount disbursed via the SR&ED program. For more details, please review our summaries of previous federal budgets.

The government reasoning for the changes is as follows:

Improving Support for Small, Growing Companies

The Scientific Research and Experimental Development (SR&ED) Tax Incentive Program encourages business innovation by providing an investment tax credit for businesses of all sizes, in all sectors, that conduct scientific research and experimental development in Canada. In a global economy where knowledge and ideas are key, the innovation of Canadian firms will be a competitive advantage. The SR&ED Tax Incentive Program is often cited as a significant source of support by Canada’s innovative firms, as it provides a 35-per-cent refundable tax credit to eligible small and medium-sized businesses and a 15-per-cent tax credit to all businesses performing SR&ED in Canada. Access to the 35-per-cent rate is determined by a business’ level of income and capital.

One challenge often cited by entrepreneurs who use the SR&ED program to grow their firm relates to how the incentive changes based on the growth of their business.

To better support growing innovative businesses as they are scaling up, the Government proposes to eliminate the income threshold for accessing the enhanced credit. This will ensure continued enhanced support for small and medium-sized innovative businesses that are experiencing rapid growth in income or may have variable income from year to year; that is, at the exact time when continued Government support can help take a business to the next level. The capital threshold will continue to apply to ensure that the enhanced rate remains targeted toward small and medium-sized businesses. This change will build on other major initiatives put forward by the Government to help make Canada a leader in science and innovation, creating the jobs of tomorrow and building globally leading businesses 45.

What is the impact?

This is perhaps one of the most expensive proposed changes in the budget over the projected 5-year period. It is estimated that it will increase government spending by $395 million, which is only dwarfed by the Canada Training Tax Credit ($815 million).

Table 1 – Federal Budget 2019